Willem Veldhuyzen

Willem Veldhuyzen No Comments

No Comments Jul 16, 2026

Jul 16, 2026Key Takeaways

- File the past due tax return now even without payment — the failure-to-file penalty compounds faster than failure-to-pay

- Prioritize refund years first — the three-year refund rule closes permanently even when no tax balance is owed

- E-file when available for faster processing; use certified mail with return receipt when paper filing is required

- Request first-time abatement or reasonable cause penalty relief after filing if your compliance history supports it

- PriorTax specializes in past due tax returns, filing 2023 taxes accurately and affordably with transparent pricing and no hidden fees

Missed the 2023 tax deadline and not sure what to do next?

Understanding how to file 2023 taxes late starts with one rule that saves money fast: file first, then deal with payment.

This guide explains what counts as a late filing, how to gather records, how penalties work, and what to do if the IRS already took action.

What “Filing 2023 Taxes Late” Means (And Why You Should File Now)

A 2023 return becomes a past due tax return after the original filing deadline, usually mid-April 2024, or after the extended deadline, usually mid-October 2024 if you filed Form 4868 for an extension.

An extension gives more time to file, not more time to pay, which matters because unpaid tax can still trigger interest and penalties after April.

Filing now matters even if your bank account is short.

The IRS failure-to-file penalty is generally much steeper than the failure-to-pay penalty, so sending the return quickly often cuts the most expensive part of the delay.

Three outcomes are common. You may be due a refund, you may owe tax, or the IRS may have built a substitute return using income reports such as Form 1099-K and wage data, often without your deductions or credits.

Federal filing comes first in this guide because IRS penalties usually drive the biggest immediate risk. If you qualify, IRS Free File or a prior-year platform can still help you complete the return, but state filing usually requires a separate step.

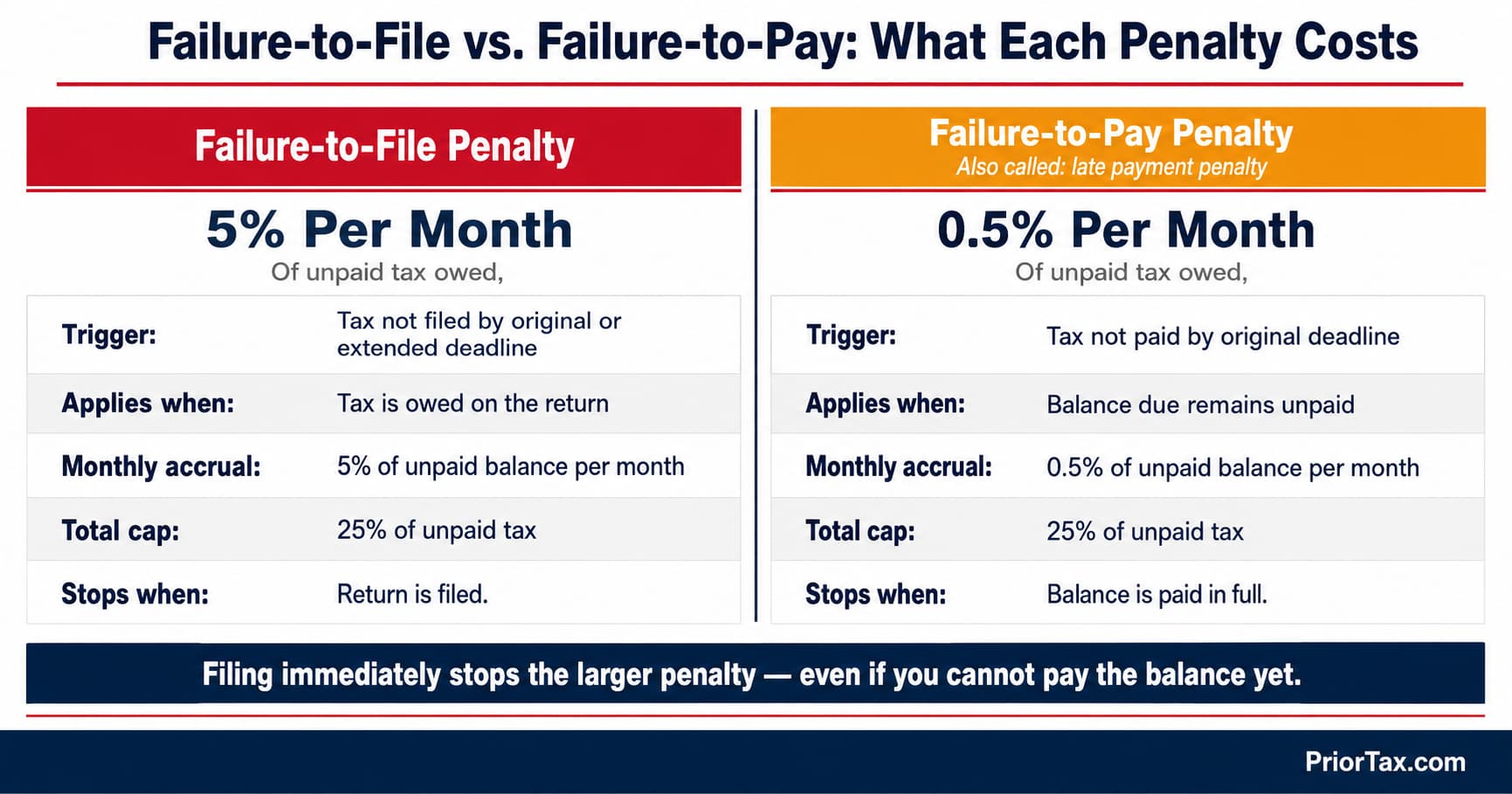

Late Filing vs Late Payment

Late filing and late payment sound similar, but they do not cost the same. The IRS generally charges 5% per month for failure to file when tax is owed, while failure to pay is commonly 0.5% per month, plus daily compounding interest.

That difference changes the strategy.

Even if you cannot pay the full bill, filing protects deductions tied to records like Form 1098 mortgage interest and stops the filing penalty from growing month after month.

Before You Start: Confirm What’s Missing and Gather Your Tax Documents

Start by confirming which years are unfiled and whether the IRS has already posted a balance due or mailed notices. An IRS online account shows account activity, and that visibility helps you avoid filing the wrong year or missing an enforcement deadline.

Gather every 2023 record you can find. T

hat usually includes a W-2, Form 1099-NEC, other 1099 series forms, Form 1098, K-1s, childcare records, receipts, and documents tied to credits such as the Earned Income Tax Credit.

Missing paperwork does not mean you are stuck.

IRS transcripts, employer payroll records, and bank statements can rebuild a return well enough to file accurately and reduce the chance of a mismatch notice later.

If records are missing, request them directly or use Form 4506-T where needed to obtain transcript information.

Taxpayers who filed Form 4868 but never finished the return should still use the original 2023 forms and instructions, not current-year forms.

Use IRS Transcripts When You’re Missing W-2s or 1099s

Request a wage and income transcript and an account transcript.

The first shows information returns reported to the IRS, while the second shows payments, notices, and whether the IRS assessed tax on your account.

Those transcripts are often enough to finish a federal return with a prior-year filing platform. They may not include every state-specific detail, so state returns sometimes require direct copies from employers or payers.

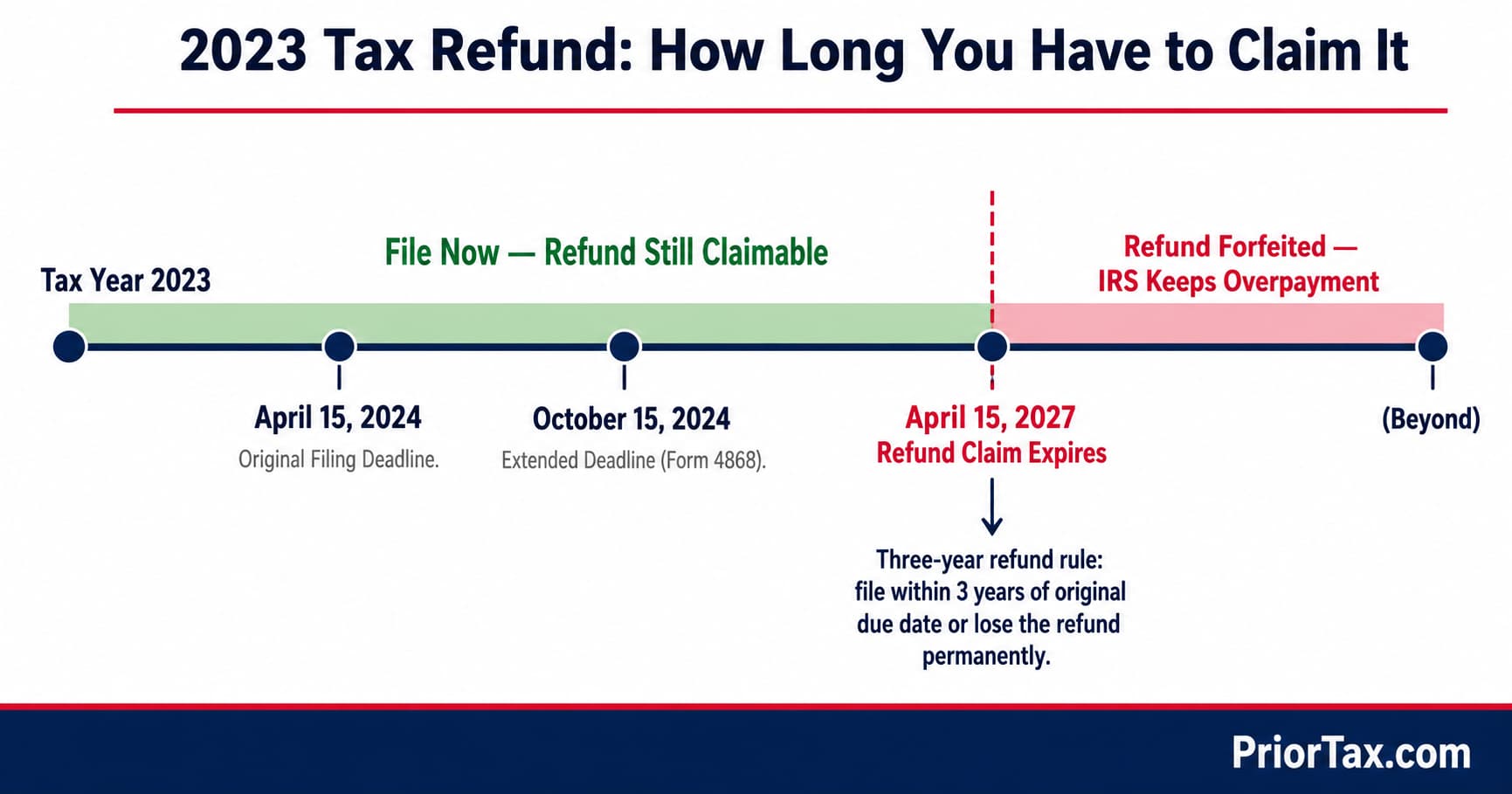

Know the Refund Deadline Rule

Refunds do not stay available forever. Under the three-year refund rule, you generally must file within three years of the original due date to claim money back, which is why delay can turn a refund into a permanent loss.

That deadline gives refund cases urgency, not flexibility. Services such as PriorTax focus heavily on older-year filing for this reason: once the refund window closes, the IRS usually keeps the overpayment.

Step-by-Step: How to File a Late 2023 Federal Tax Return

Choose the filing method first.

If e-file is still open for 2023 through an approved provider like PriorTax, use it because electronic filing is faster, creates a timestamp, and reduces transcription errors that often trigger IRS notices. E-file for 2023 tax returns will close this year (2026) in late November to late December, depending on when the IRS decides to shut down their e-file system for the year.

Complete Form 1040 and every schedule that applies to your situation.

Self-employed taxpayers may need Schedule C, investors may need Schedule D, and many filers miss tax credits because they rush past dependent, education, or premium tax credit questions.

Check the details that cause the most rejected or adjusted returns. Filing status, Social Security numbers, direct deposit data, withholding, and dependent eligibility produce a large share of avoidable IRS corrections.

Submit the return and keep proof.

E-file acceptance records matter, and paper filers should use certified mail with return receipt because proof of mailing can settle future disputes about whether the IRS received the return.

E-File vs Mail: What to Use for a Past-Due 2023 Return

E-file is usually the better option when available. Processing is quicker, math checks are automatic, and the IRS can acknowledge receipt within hours instead of weeks.

Paper filing still works if e-file is closed or unsupported.

Use the IRS address for your state, attach all schedules and W-2 copies, and keep a full copy of what you mailed.

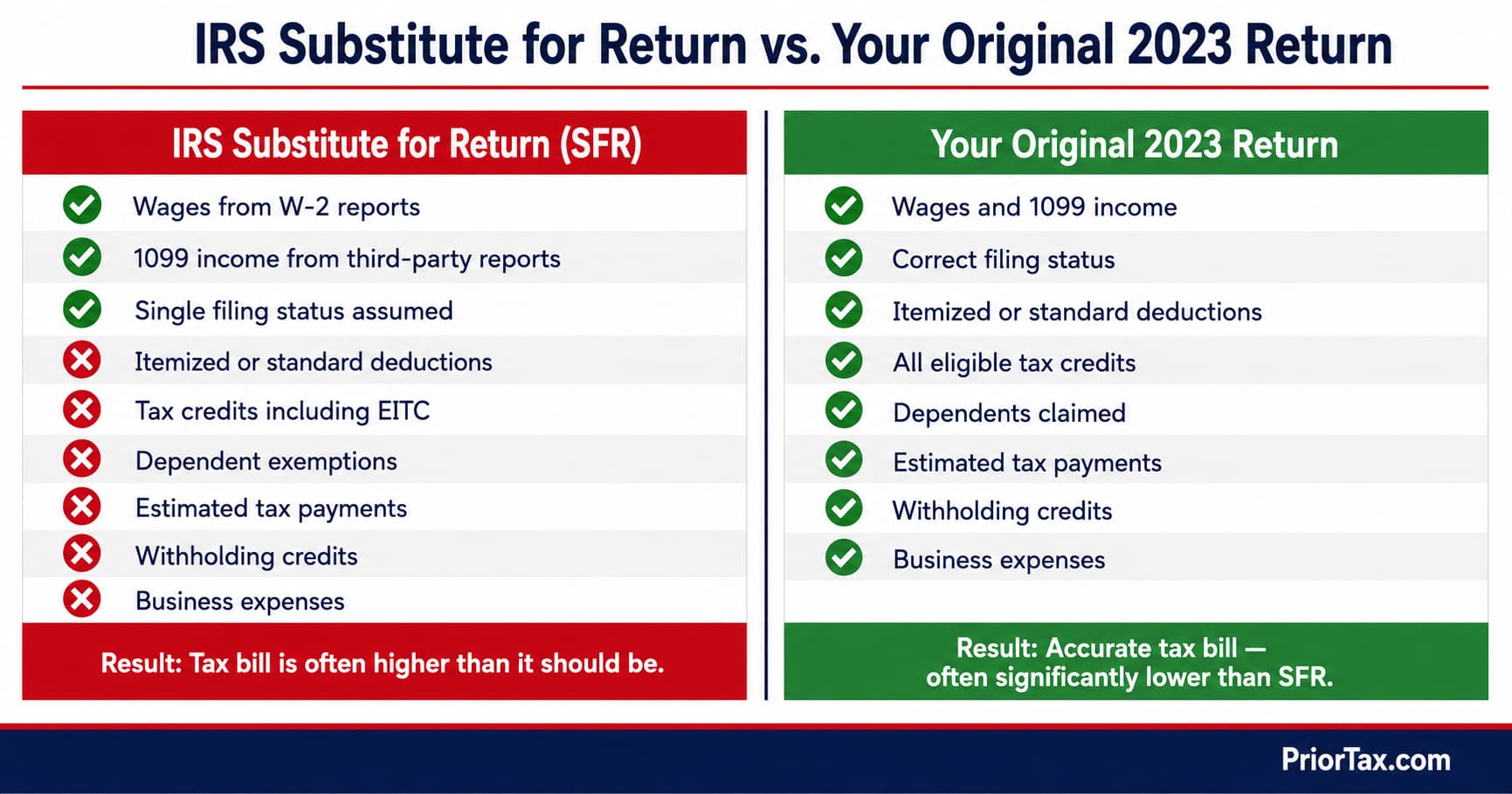

If the IRS Filed a Substitute for Return (SFR)

An SFR is the IRS version of your return built from third-party data.

It often leaves out credits, business expenses, filing status changes, and dependents, which can make the tax bill much higher than it should be.

You can usually replace that SFR by filing your original 2023 return.

Accurate original filing is one of the fastest ways to cut an inflated assessment and restore credits the IRS never included.

What Happens If You File Late: Penalties, Interest, and Enforcement

If you owe tax, the IRS commonly charges a failure-to-file penalty of 5% per month up to 25% of the unpaid tax.

The failure-to-pay penalty is commonly 0.5% per month, and interest accrues on both tax and some penalties.

Interest compounds daily, which means delay becomes more expensive even when the monthly penalty looks modest. Small balances can grow faster than people expect because the IRS keeps adding charges until the account is resolved.

If you are due a refund, late filing usually does not trigger the late-filing penalty. The real risk is losing the refund entirely after the claim window closes.

Long non-filing periods can lead to collection notices, federal tax liens, bank levies, and wage garnishment. Serious enforcement usually follows repeated nonresponse, which is why filing is often the move that slows escalation first.

If You Owe vs If You Don’t Owe

Taxpayers who owe should expect penalties and interest to continue until the return is filed and payment arrangements are active.

Filing changes the case from noncompliance to debt resolution, and the IRS treats those situations differently.

Taxpayers due a refund should still file quickly.

An open tax year can block credits, delay future compliance, and leave money unclaimed for no good reason.

If You Can’t Pay: Smart Options to Reduce Damage After Filing

Pay something immediately, even if it is small.

Partial payment reduces the balance subject to interest and penalties, which makes every later payment more effective.

Then look at formal IRS payment options.

An installment agreement with the IRS is the standard path for people who can pay over time, while an Offer in Compromise is reserved for taxpayers whose finances show they likely cannot pay the full amount before collection limits expire.

Penalty relief may also be available. First-time abatement can help taxpayers with a clean compliance history, while reasonable cause relief applies when facts such as illness, disaster, or destroyed records can be documented.

Taxpayers who need structured help can review resources on filing 2023 taxes late or seek help with late tax filings. The right plan depends less on the tax bill alone and more on whether your income can support monthly payments.

Installment Agreement Basics (Form 9465)

Most long-term payment plans require the return to be filed first.

Form 9465 is the standard request for an installment agreement, and the monthly amount should fit your real budget because missed payments can default the plan.

A realistic payment plan beats an aggressive one that collapses after two months. IRS collections usually get harsher after default, not more flexible.

Penalty Relief and When It Applies

First-time abatement may apply if you filed and paid on time in prior years and have no major recent compliance problems.

That relief is administrative, not automatic, so you may need to request it.

Reasonable cause relief requires facts and proof. Hospital records, insurance claims, police reports, or disaster documentation carry more weight than a general statement that life got busy.

State Taxes: Don’t Forget the Separate Deadlines and Penalties

State returns are separate from federal returns, and many taxpayers need to file both even when they cannot pay either bill immediately.

That split matters because a filed federal return does not satisfy a state filing requirement.

States set their own penalty rates, interest rules, and collection tools.

New York, for example, publishes separate guidance for late filing, late payment, and penalty calculations, which shows why copying a federal strategy to a state case can create mistakes.

Residency can complicate late filing. Taxpayers who moved during 2023 may need part-year returns or multiple state filings, and wage allocation errors can trigger notices from both states.

How to Prioritize Federal vs State When You’re Behind

File both as soon as possible if you can.

If time or records are limited, start with the return carrying the highest enforcement risk or the nearest refund expiration.

Keep income figures consistent across systems.

IRS transcripts, employer payroll records, and state withholding data should line up, or one agency may flag the mismatch before the other does.

Common Mistakes When Filing a Late 2023 Return (And How to Avoid Them)

The costliest mistake is waiting until you can pay in full.

Filing late adds avoidable penalties, while filing now and paying later usually lowers total damage.

Another common error is using the wrong year’s forms. A 2023 return must use 2023 rules, 2023 credit amounts, and 2023 worksheets, or the math around withholding, credits, and taxable income can break quickly.

People also forget withholding and estimated tax payments.

That oversight can wildly overstate what you owe because the IRS may not credit every payment correctly unless the return reports it clearly.

Proof matters. Taxpayers who cannot show e-file acceptance or mailing records often struggle to fight a later IRS claim that the return was never received.

Document and Math Checks That Prevent Notices

Names, Social Security numbers, and dependent details should match Social Security Administration records exactly. Credit claims fail often because one digit is wrong or a child was claimed by the wrong taxpayer.

Bank routing and account numbers deserve a final review before submission.

Direct deposit errors delay refunds, and correction after filing is much harder than checking once more before you send it.

Quick Examples: What to Do in Common “Late 2023 Taxes” Situations

A refund case is the simplest.

File as soon as possible because the three-year deadline can erase your claim even when the IRS owes you money.

An unpaid balance case needs a different order.

File first, pay what you can now, then request a payment plan so the IRS sees active compliance instead of continued silence.

Missing forms are common, especially for gig workers and contractors.

Pull transcripts, ask the payer to reissue the W-2 or 1099, and use those records to complete the return accurately.

An IRS notice or SFR changes the urgency. File a correct original return quickly because replacing an inflated IRS substitute assessment can cut the balance more than any payment strategy alone.

What “Compliance” Means If You Have Multiple Unfiled Years

The IRS often expects the most recent six years to bring a taxpayer into compliance in many collection situations.

That practice is not the same as a legal limit, because if a required return was never filed, the statute of limitations generally does not start.

Old years stay open until a real return is filed. That is why back-tax cleanup should begin with the years tied to active notices, refund deadlines, or the largest balances.

FAQs

Can I still file my 2023 tax return?

Yes. You can still file a 2023 return after the deadline. Filing promptly helps stop the failure-to-file penalty from growing and protects any refund still within the claim window.

What happens if I forgot to file taxes for 2023?

If you owed tax, penalties and interest may keep accruing until you file and pay or set up a plan. If you were due a refund, you usually will not face a late-filing penalty, but you can lose the refund if you wait too long.

How do I file a late 2023 tax return?

Gather your 2023 records or use IRS transcripts, complete Form 1040 and any required schedules, then e-file if available or mail the return. Keep proof of filing and arrange payment if you owe.

Can I still file my 2023 taxes on TurboTax?

Often, yes, because many software providers support prior-year returns for a period of time. If e-file is unavailable, you may need to print and mail the return or use a provider that still supports late-year e-filing.

Filing a late 2023 return is mostly about sequence. Send the correct return first, preserve your refund or cut the filing penalty, then solve the balance with payments or relief options that fit your facts.

Categories: